English

English16469

|

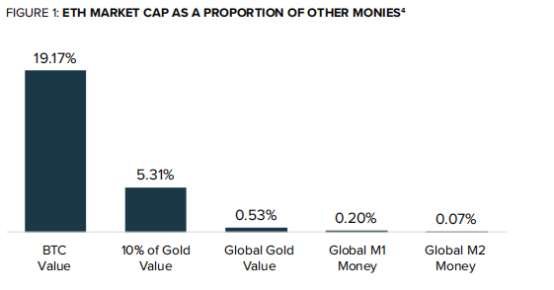

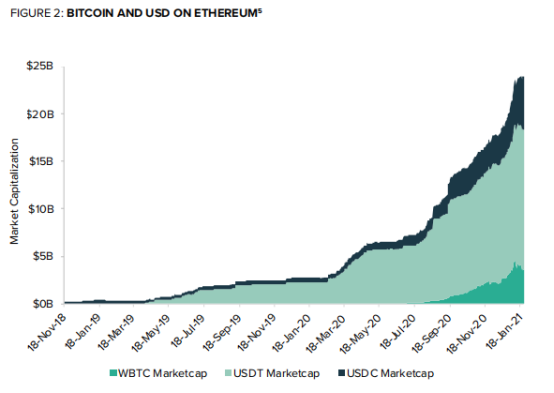

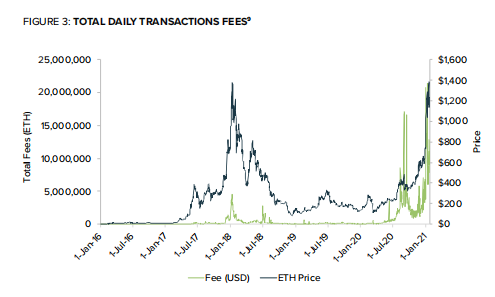

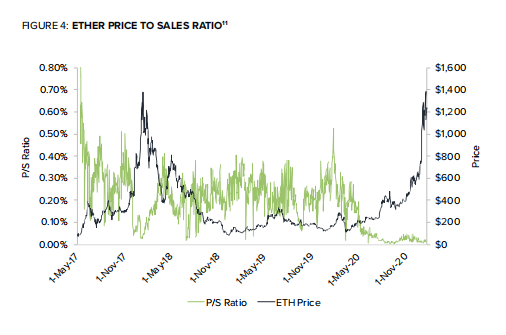

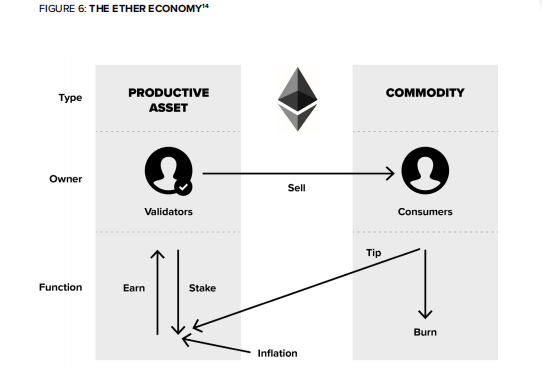

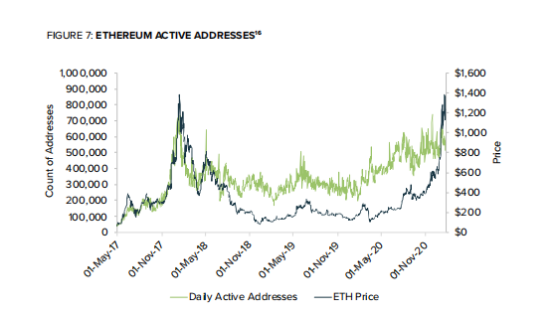

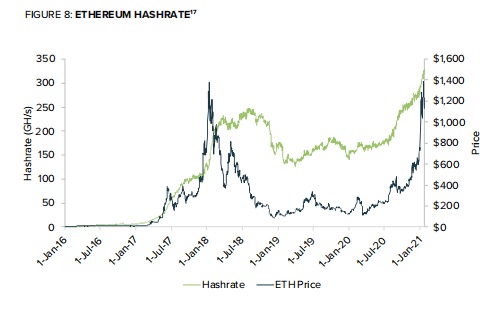

Since its birth in 2015, Ethereum has attracted great interest from investors as the second largest blockchain network. Even as the network matures into a powerful settlement layer for billions of dollars of peer-to-peer value transfer, investors often struggle to identify the investment case. Bitcoin's value proposition is the promise of a globally verifiable accounting system, supported and guaranteed by the world's most powerful computing network, where users can track value with a high degree of confidence. The emergence of Ethereum also promotes the development of verifiable systems, but achieves a wider information scope and logic. In other words, Ethereum’s powerful network ensures that applications can run according to coded logic without third-party intervention and without interference. Ethereum creates a trustworthy environment, which has historically been a prerequisite for prosperous transactions. Does this mean Ethereum is better than Bitcoin? Not necessarily, they specialize in different frontier directions and make corresponding trade-offs. Bitcoin is rock solid but lacks flexibility. Investors always believe that its accounting system will not change arbitrarily. ; Ethereum is more flexible and can build an innovative and iterative environment. Ethereum and Bitcoin enjoy a symbiotic relationship, drawing liquidity, share, and value from the outside world. Bitcoin is the preferred store of value in the digital ecosystem, while Ethereum has become the leading financial infrastructure, settling over $12 billion in daily transactions. With more and more activity on the Ethereum mainnet, investors are eager to know about investment cases and the valuation of ETH, the native asset of the Ethereum network. In August, Grayscale released a report on Bitcoin valuation to help investors understand the investment case for Bitcoin and how they can look at important fundamental indicators. Likewise, while Bitcoin is widely referred to as digital gold, while ETH’s designation is less clear-cut, we outline important considerations for ETH valuation by exploring three approaches and the metrics associated with each approach (ETH as currency, consumable, or interest-earning asset). 1. ETH as currency ETH is the native asset that supports the DeFi system and is used as minimal collateral for lending trust. At the time of writing, there are approximately 7 million ETH locked as collateral in the decentralized protocol on the Ethereum network, worth over $9 billion at current prices. In other aspects, ETH plays an important role on the Ethereum network as a new era digital currency. Whenever users deploy smart contracts on the Ethereum network, provide liquidity for applications, or conduct transactions on DEX, ETH is also used to pay network fees. While the Bitcoin community believes that the supply of money should be a fixed amount, Ethereum issues the minimum necessary amount in order to fully secure the network. While the fixed supply is the main highlight of Bitcoin, ETH's use as a currency is driven by applications on the Ethereum network. For Ethereum, application scenarios drive the value of ETH as a currency commodity on the Ethereum network.  Figure 1: ETH market value share ETH’s use as collateral in the DeFi ecosystem continues to expand. However, the rising usage of stablecoins (digital currencies primarily pegged to the U.S. dollar) and Bitcoin as collateral on the Ethereum network may challenge ETH’s status as the ecosystem’s preferred collateral. WBTC is a synthetic version of Bitcoin on Ethereum, which allows Bitcoin to be transferred on the Ethereum network. USDT and USDC are the largest USD stablecoins on Ethereum. The chart below shows the growth of WBTC, USDC, and USDT. While the growth of alternative assets on the Ethereum network may challenge the use of ETH as collateral, the increased use of Ethereum as a settlement network is a positive trend.  Figure 2: Bitcoin and USD on Ethereum 2. ETH as a consumable ETH is an important part of the operation of the Ethereum network. Every transaction on the network has a cost, which is priced in ETH, and these transaction fees are then distributed to miners. Fees will increase as network demand increases, and transactions must "compete" for space in specific blocks by increasing the associated fees. Some analysts pointed out that it may not be necessary to use ETH to pay fees, but to choose any digital currency to pay fees and use it to challenge the value of ETH. This is called abstract economy. Similarly, some people believe that ETH has working capital or network speed issues. As a medium of exchange asset, investors may seek to minimize holdings only to pay for a certain service. In other words, ETH will be regarded as working capital. Because investors may seek to minimize working capital, the network speed of ETH will increase, but the price of ETH may decrease based on the trading formula M=PQ/V. However, Ethereum plans to implement a proposal called EIP-1559, which will burn (or destroy) the ETH used to pay for transactions. This proposal will transform ETH from a medium of exchange asset into a consumable commodity, making ETH more like a flammable gas than a currency. If this proposal is implemented, it will ensure that ETH is the native economic unit on the Ethereum network. The protocol rules determine that only ETH can be burned. Using ETH for payment will reduce the possibility of economic abstraction. This burning method can also serve as a deflationary mechanism if more ETH is consumed than planned issuance.; If activity increases and the supply of ETH decreases, the supply and demand curve will be reflected in an increase in the price of ETH units. ; If EIP-1559 is implemented, it will establish a consumption mechanism and form a positive feedback loop for ETH prices. As a commodity, the price of ETH fluctuates based on supply and demand in the market. Fortunately, the Ethereum blockchain is transparent and user activity can be analyzed to explain a fair potential market price for ETH. We can use the total daily transactions collected on the Ethereum network as a measure of demand, as shown in the chart below. Since ETH is a commodity that pays fees, high fees drive demand for ETH, just as increased frequency of travel may drive demand for GAS. Notably, total transaction fees in January 2021 were 5 times the peak fees in January 2018. However, Ethereum’s price is roughly equivalent to its 2018 peak.  Image 3: Total daily transaction fees Transaction fees are the total amount paid for an exchange on the Ethereum network. Another way to think about the value of ETH is to compare the historical price of ETH to the transaction fees generated by the network. The chart below illustrates this relationship using the Price to Sales (P/S) ratio – a lower ratio indicates that transaction fees are high relative to ETH’s historical price and the Ethereum network is generating higher revenue. This means that there is a possibility that ETH is undervalued.  Image 4: ETH price to sales ratio We can learn about the situation on the ETH supply side by checking the holding pattern. In the Bitcoin Valuation Report, we quoted the “Hodler – Speculators” index, which designates assets belonging to Hodler as assets that have not moved in 1-3 years, and assets belonging to speculators as assets that have moved in the past 90 days. Although the Ethereum network is still too young compared to Bitcoin and the specific behavior pattern is not particularly clear, it can still be seen that Hodler's assets peaked before ETH gained 300% in 2020. Using traditional investment analysis frameworks, it can be useful to look at supply patterns.  Image 5: Hodler and speculators 3. ETH as an interest-bearing asset Ethereum 2.0 is starting a new phase of Ethereum and aims to be a scalable proof-of-stake blockchain. This means that miners no longer need to expend energy through dedicated computers to mine, but instead receive rewards by staking ETH to become a validator on the Ethereum network. Validators will receive a portion of the transaction fees (fees may be burned according to EIP-1559) and receive a proportion of the additional ETH issuance caused by the inflation of the Ethereum network. This is another key shift in thinking about the value of ETH. Ethereum 2.0 will transform Ethereum from a commodity to a productive commodity - holders will be able to generate interest through staking. This asset structure is unlike any other in the physical world. As we all know, goods can be consumed and stocks provide rights to cash flow. Under the framework of Ethereum 2.0, ETH can be consumed as a commodity or as a claim on cash flow, similar to equity. Its initial value is derived from its commodity use and market supply and demand dynamics. Investors who are confident in the future price prospects of ETH can earn profits by betting on ETH. This could further reduce the floating supply of ETH. If a large amount of ETH is staked, this will reduce the supply available for consumption, creating a positive feedback loop for the price of ETH. See the table below to understand how value flows through the Ethereum 2.0 network. Keep in mind that the launch date for the fully functional Ethereum 2.0 network has not yet been determined.  Picture 6: ETH economic mechanism Other indicators The number of daily active addresses is a very useful metric for measuring network growth. According to Metcalfe's law, the value of a network is proportional to the square of the number of users (this law was originally used to measure the value of Facebook). Currently, Ethereum has nearly 700,000 active addresses every day.  Picture 7: Ethereum active addresses The hash rate on Ethereum has also reached new heights. Since it takes time for miners to recoup their initial investment, rising hash rates mean miners are confident that Ethereum will continue to generate high profits. If miners believe that transaction fees will decrease, they will be less willing to allocate resources to mining activities.  Image 8: Ethereum hash rate changes and ETH price changes Ethereum is younger than Bitcoin and continues to undergo major changes. As a result, the methods for valuing the underlying asset ETH are opaque and constantly changing. Treating ETH as a currency, consumer product, or interest-bearing asset allows investors to consider a range of possible outcomes when assigning a fair value to the asset. The EIP-1559 proposal will improve the asset structure of Ethereum and convert ETH into consumer goods by burning tokens, which will become a catalyst for the value of ETH. The proposal also supports ETH as a native asset of the Ethereum protocol, reducing the validity of previous analysis that assumed ETH could be removed from the ecosystem. Finally, if Ethereum 2.0 is successfully realized, investors are expected to use Ethereum as an interest-bearing asset and continue to generate income through staking. Ethereum’s massive on-chain activity, economic improvements, and Ethereum 2.0 scalability… there’s a lot for the Ethereum community to be excited about. We can observe from the data that ETH price tends to move in response to underlying activity on the network. As noted in this report, multiple Ethereum metrics are reaching new highs, including active addresses, hash rate, and network fees—a positive sign for investors. Let’s make an introduction about Ethereum in the past few years: At the end of 2013, Ethereum founder Vitalik Buterin released the first version of the Ethereum white paper and launched the project. Starting from July 24, 2014, Ethereum conducted a 42-day Ethereum pre-sale. In early 2016, Ethereum's technology was recognized by the market and its price began to skyrocket, attracting a large number of people other than developers to enter the world of Ethereum. Huobi and OKCoin, two of China's three major Bitcoin exchanges, both officially launched Ethereum on May 31, 2017. Since the start of 2016, those who follow the digital currency industry closely have eagerly watched developments in the second-generation cryptocurrency platform Ethereum. As a relatively new development project utilizing Bitcoin technology, Ethereum is committed to implementing a global decentralized and ownership-free digital computer to execute peer-to-peer contracts. Simply put, Ethereum is a world computer that you cannot turn off. The innovative combination of cryptographic architecture and Turing completeness can promote the emergence of a large number of new industries. In turn, traditional industries are under increasing pressure to innovate and are even at risk of becoming obsolete. The Bitcoin network is actually a set of distributed databases, while Ethereum goes one step further. It can be regarded as a distributed computer: the blockchain is the ROM of the computer, the contract is the program, and the miners of Ethereum are responsible for calculations and play the role of CPU. This computer is not and cannot be free to use, otherwise anyone can store all kinds of junk information in it and perform all kinds of trivial calculations. Using it requires at least paying computing fees and storage fees, and of course there are other fees. The most well-known is the Enterprise Ethereum Alliance established in early 2017 by more than 20 of the world's top financial institutions and technology companies, including JPMorgan Chase, Chicago Exchange Group, Bank of New York Mellon, Thomson Reuters, Microsoft, Intel, and Accenture. Ethereum, the cryptocurrency spawned by Ethereum, has recently become the most popular asset after Bitcoin. Ethereum is an open source public blockchain platform with smart contract functions. It provides a decentralized Ethereum Virtual Machine (Ethereum Virtual Machine) to process point-to-point contracts through its dedicated cryptocurrency Ether (ETH). The concept of Ethereum was first proposed by programmer Vitalik Buterin between 2013 and 2014 after being inspired by Bitcoin. It roughly means "the next generation of cryptocurrency and decentralized application platform" and began to develop through ICO crowdfunding in 2014. |

|

|

|

|

|