English

English71135

|

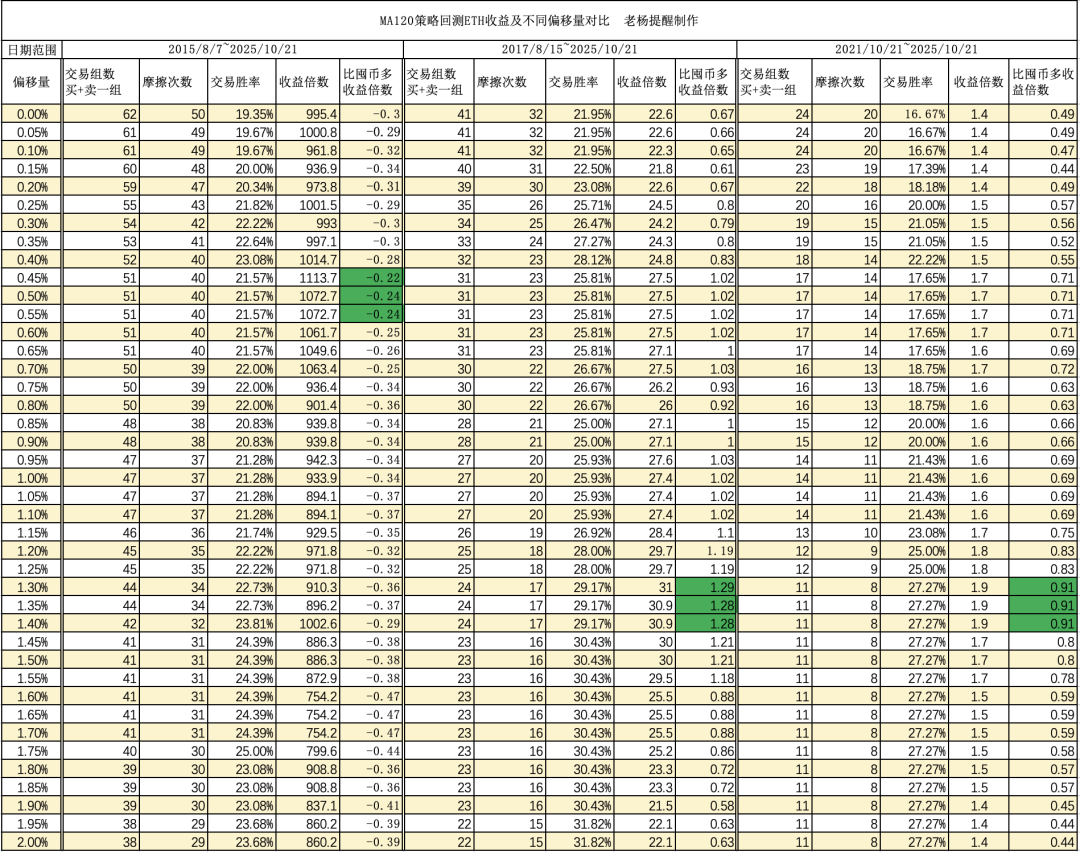

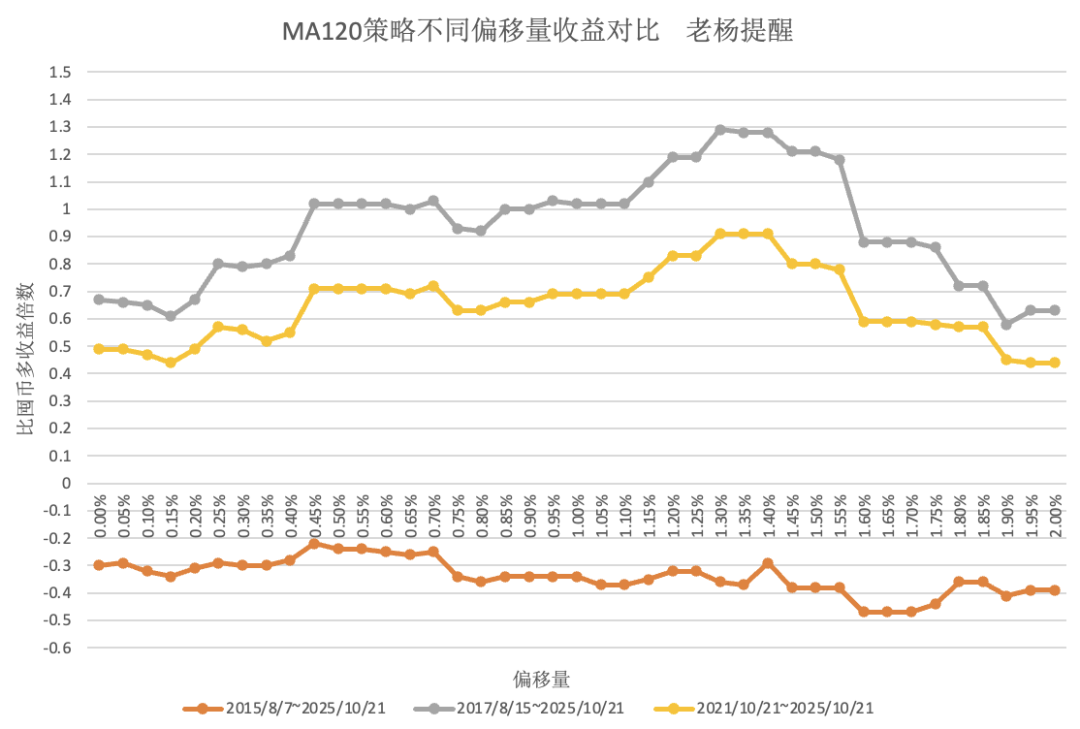

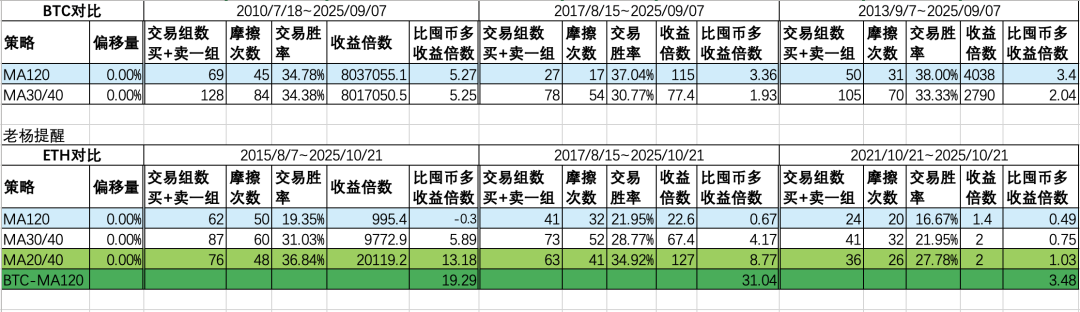

After I wrote the BTC article "How to Sell - MA120 Strategy Backtesting and Offset Settings" last time, many friends wanted me to calculate ETH, so I came up with this article. 1. Let’s talk about the difficulties in executing MA120 again First of all, I would like to talk about the difficulties in executing MA120, because there has been a lot of friction recently, especially without adding an offset. Even if you are confident when you want to implement this strategy, repeated wear and tear can exhaust your confidence, especially when others are gossiping about it, which will make you not want to implement it. So think clearly about this strategy, which is to exchange small wear and tear for big results. You must think clearly before you want to use it, and you must implement it to the end, at least stop when big results appear. Don't avoid the wear and tear, but miss the big meat. There are only two core objectives of the strategy 1) You were there when the price surged; 2) You escaped when the market fell sharply. Another point is position control. Don’t use large positions as soon as you start. I am currently holding about 20 to 30% of the positions, and my mentality is okay. Even for selling, sometimes the wear and tear has to go back and forth many times, so it's better to do it with a program. Now that AI is so advanced, it is not difficult to write a program for it. 2. ETH’s MA120 strategy backtest 1. Time setting This is similar to BTC Full time period data 2015/7/18~2025/10/21 But considering the early price distortion, the second backtest Binance has data starting from 2017/8/15~2025/10/21 Let’s consider a period that goes back four years from now, from 2021/10/21 to 2025/10/21, because a four-year cycle 2. Parameter setting (same as BTC) lookTransaction win rateNo matter what, just forget itNumber of friction, consider buying and selling as a group to calculate friction, so set aNumber of trading groups(buy and sell transactions twice as a set) concept. The starting capital is set to 1, and the handling fee is set to 1,000.The reference standard is hoarding coins, take 1u each at the starting point, one portion is used to run MA120, and one portion is used to hold it still. Let's run this down. For example, the current market value of MA120 is 100, and the market value of hoarding currency is 20, then the market value of MA120revenue multipleis 100/1=100,Multiples of profit than hoarding coins=100/20-1=4 Offset concept, when it rises, it exceeds the closing price of MA120, and when it falls, it is lower than the closing price of MA120. consideroffsetAssume how much is appropriate and traverse 0, 0.05%, and 0.1%. . . . 2%, 3. Backtest results  What are the benefits of the ETH-MA120 strategy? The full cycle data basically cannot outperform hoarding currency, and is about 30% lower than hoarding currency. In the 8 years that Binance has data, the income is only 0.6 to 1.3 times higher than that of hoarding coins. In four years, the income is only 0.4 to 0.9 times more than hoarding coins. In the same period, BTC had about 3 to 5 times the profit, which is a bit different. In comparison, the main reason is that the winning rate of ETH is lower, about 20%, and the profit is basically wiped out, while that of BTC is about 30%. 4. How to set the offset In order to compare the various offset results more intuitively, I drew the above table as follows:  The full cycle offset is 0.45% optimal, and the other two cycles are 1.3% optimal. The pattern is not so obvious. 3. What is the MA120 signal of ETH using BTC? ETH has too much friction, can I use BTC indicators? The MA120 strategy verification is also based on "a multiple of profit compared to hoarding coins" as the benchmark:

in conclusion:It is better for ETH to refer to BTC's MA120 at all times. Then it is based on the signal of BTC, and it is simple to execute. 4. Which strategy is better, MA120 or MA30/40? Last time I compared BTC’s MA120 and MA30/40, the conclusion is that BTC’s MA120 is better.  Comparing it with ETH, we find that it is completely the other way around. The income is MA20/40>MA30/40>MA120. Then use it with ETHWhat about BTC’s MA120 signal comparison? The result is: using BTC's MA120 signal is more advantageous, not only exceeding ETH's own MA120, but also exceeding MA20/40 and MA30/40. Is the conclusion obvious at this point?For both BTC and ETH, just use BTC's MA120 signal to run. 5. Comprehensiveness of data First, backtests are all based on historical data. Actual future trends can only be predicted and cannot be completely simulated. Second, this single MA120 parameter cannot cover the entire market. The returns may be very good or very poor. If you want to obtain stable and relatively good returns, you should consider more parameters. This is what Mr. Nian @王宁 explained to me. Thank you. For example, if MA30, MA120, and MA200 are used at the same time, it will be relatively stable. In actual operation, I will use part of the position to trade BTC and ETH, and use the MA120 signal of BTC uniformly. Take another position and trade ETH, use its MA20/40, and run without adding an offset. Therefore, each strategy is for reference only. If you want to use it, you still have to find a way to implement it comfortably. This is the key point. I wish you fortune! |

|

|

|

|

|