English

English50547

|

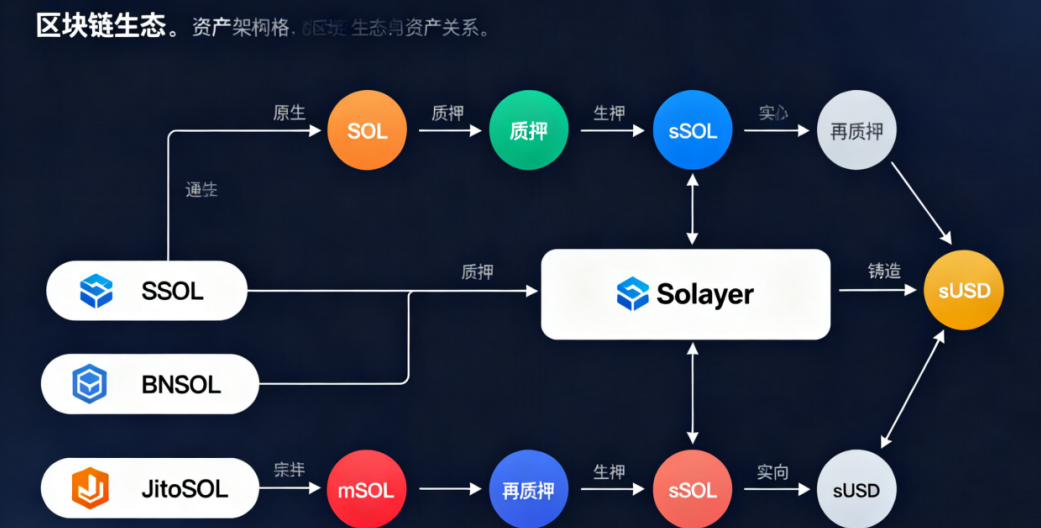

1. The core of the event: Solana’s first RWA stablecoin started casting, unlocking multiple rights and interests At 22:00 on October 30, 2025, Beijing time, Solayer, the leading re-staking platform of Solana ecosystem, officially opened the casting of its first synthetic stablecoin sUSD supported by RWA (real world assets). This action marks Solana’s breakthrough progress in the field of real asset tokenization. According to the official rules, the upper limit of the first batch of sUSD minting is set at 20 million US dollars. In order to activate the early market, users can enjoy 10 times the reward rights for the first 10,000 US dollars of minting amount. ; More importantly, sUSD comes with the dual attributes of "income + pledge" - users can obtain 4.33% annualized on-chain income by holding it (the income comes from the interest distribution of the underlying US Treasury bond RWA token). At the same time, like the platform's native asset sSOL (the liquid token that pledges SOL), it can be used as a pledge asset for the Solana network verification node, providing economic support for network security and stability. As a stablecoin issued based on the Solana Token2022 standard, sUSD has been different from traditional stablecoins since its birth: Token2022's "interest-bearing token" native function allows revenue distribution to be automatically executed directly through the protocol layer without relying on third-party contracts, reducing contract risks.; The "transfer hook" feature reserves technical space for subsequent transaction fee adjustments and revenue rule optimization. Combined with Solana's 5000+TPS throughput and transaction costs of less than $0.01 through the Firedancer client upgrade, sUSD has the efficient processing capabilities for high-frequency RWA transactions.  2. Innovation Trio: Reconstructing the Value Logic of Stablecoins 1. RWA collateral: dual anchoring of compliance and income sUSD chooses U.S. Treasury bonds as the underlying mortgage asset, accurately targeting the breakout node of the RWA track in 2025. According to the "2025 Web3 Technology White Paper", the current global RWA market size has reached US$26.4 billion and is expected to exceed US$50 billion by the end of the year, of which low-risk financial asset tokenization accounts for more than 70%. As the most liquid low-risk asset in the world, U.S. Treasury bonds provide natural value stability for sUSD in its tokenized form. ; The annualized return of 4.33% is significantly higher than the 0-2% return range of traditional stablecoins, forming a differentiated competitive advantage. More importantly, this "compliant financial assets + on-chain income" model lowers the threshold for traditional funds and low-risk appetite investors to enter Web3. 2. Ecological synergy: improve the Solayer re-staking closed loop sUSD is not an isolated product, but forms a deep synergy with sSOL, the core asset of Solayer's ecosystem. Currently, sSOL has achieved US$150 million in TVL (total locked value) through the re-pledge mechanism, ranking the 13th largest protocol in the Solana ecosystem. ; The addition of sUSD creates a complete closed loop of "SOL pledge → sSOL liquidity release → sUSD income appreciation". Users can flexibly realize the asset conversion of SOL, sSOL, and sUSD in the Solayer re-pledge pool - not only retaining the basic income of SOL staking, but also obtaining the payment function and additional income of stable currency through sUSD, which greatly improves the efficiency of fund use, while injecting more pledged assets into the Solana network and strengthening the consensus foundation. 3. Industry paradigm: Promote the implementation of RWA standardization In 2025, Hong Kong has launched the world's first RWA registration platform to clarify the access standards and operating specifications for asset tokenization, and sUSD is a typical sample of compliant RWA products. Compared with the RWA project in the Ethereum ecosystem, sUSD relies on Solana's high-performance advantages and is more suitable for high-frequency and low-cost participation by retail-level users, accelerating the popularization of RWA. ; Its model of "transparency of underlying assets + automatic distribution of on-chain income + network pledge empowerment" also provides the industry with a reusable standardized paradigm, promoting RWA from "niche pilot" to "large-scale application". 3. Ecological value: Two-way empowerment of Solana and RWA track 1. Make up for Solana’s shortcomings of “value stabilizer” For a long time, the Solana ecosystem has relied too much on the value support of SOL as a single asset. Token price fluctuations not only restrict the expansion of the ecosystem, but also increase the risks for developers and users. The launch of sUSD, with U.S. Treasury bonds, a low-volatility asset, as the anchor, fills the gap of compliant RWA stablecoins in the Solana ecosystem. It not only attracts the entry of traditional financial funds, but also provides a stable value medium for DeFi protocols and payment scenarios in the ecosystem. At the same time, it further enhances network security through the pledge function, forming a dual competitiveness of "stability + efficiency" with Solana's high-performance advantages. 2. Open the “on-chain application” space for the RWA track Traditional RWA projects mostly focus on the “on-chain link” of asset tokenization, but ignore the expansion of on-chain application scenarios.; Through the dual attributes of "revenue-based stablecoin + pledged assets", sUSD gives RWA assets actual use value - not only a value storage tool, but also a participant in blockchain network governance and security maintenance, broadening the application boundaries of RWA. This "asset on-chain + scenario implementation" model also provides a reference for other RWA projects, promoting the industry's upgrade from "asset tokenization" to "token scenarioization". 4. Risk analysis: multi-dimensional challenges to be overcome Although sUSD has a promising future, it still faces risks that overlap with the commonality of the industry and its own characteristics, which requires a rational review: 1. Risks of regulatory characterization and compliance conflicts The draft of the U.S. Stablecoin Bill may expand the definition of "endogenously collateralized stablecoins." Although sUSD claims to be collateralized by U.S. Treasury bond RWA tokens, synthetic stablecoins such as Synthetix sUSD have historically been subject to regulatory scrutiny due to the collateralization of related governance tokens. At present, the RWA regulatory framework of the US SEC and European ESMA has not yet been finalized, but Hong Kong has issued clear rules. If sUSD targets multi-regional users, it may fall into a "compliance doll" dilemma - for example, the United States requires localization of underlying asset custody, while Hong Kong emphasizes penetrating audits of cross-chain assets. Double standards will significantly increase operating costs. More importantly, the tokenization of U.S. Treasury bonds may hit the red line of "unregistered securities issuance". Pioneers such as BlackRock BUIDL have adopted registered investment company (RIC) qualifications to avoid risks, but Solayer has not yet disclosed similar compliance arrangements, leaving regulatory uncertainty. 2. Asset liquidity and maturity mismatch risk The income stability of sUSD is highly dependent on the liquidity of the underlying US Treasury bonds, but such assets have natural maturity mismatch risks. Referring to the bankruptcy case of Silicon Valley Bank, which allocated short-term deposits to long-term treasury bonds, which led to liquidity depletion, sUSD faced a similar problem: users can redeem stablecoins at any time, but if the underlying treasury bond tokens are mainly 1-3 year products, discount losses may occur during emergency liquidation. In the current on-chain RWA market, only 30% of the treasury bond tokens can be redeemed on T+1, and the rest require a 7-14 day settlement cycle. If there is a centralized redemption of the first batch of 20 million US dollars, Solayer may cause a run due to insufficient reserves. In addition, changes in the Federal Reserve's monetary policy will also impact income commitments - if the resumption of interest rate increases causes Treasury bond prices to fall and yields to fluctuate, sUSD may fall into a vicious cycle of "shrinking income → user redemptions → tight liquidity". 3. Technology adaptation and network security risks As a new protocol in the Solana ecosystem in 2025, the Token2022 standard still lacks stress testing for large-scale applications. Its "interest-bearing token" module needs to be accurately synchronized with the semi-annual interest payment cycle of U.S. Treasury bonds, but the automatic execution mechanism on the chain has not yet been verified across cycles, and there may be deviations in income calculation or distribution delays. ; At the same time, although the Solana network has improved throughput through Firedancer, it has experienced many interruptions due to node synchronization issues in history. If sUSD is used as a pledged asset to access verification nodes on a large scale, network failures may cause pledge rewards to be suspended and asset redemptions to be stagnant, forming a transmission chain of "technical risk → ecological trust crisis". 4. Ecological chain risk: systemic risks of the re-pledge system The deep synergy between sUSD and sSOL increases the ecological value, but also amplifies systemic risks. About 40% of the current USD 150 million TVL of sSOL has been used for cross-protocol re-pledge. If sUSD is unanchored due to the above-mentioned risks, it will trigger a crisis of trust in the entire Solayer re-pledge system, leading to a concentrated sell-off of sSOL. In 2024, a certain project in the Ethereum ecosystem was de-anchored due to a stablecoin, causing the associated pledged tokens to fall by more than 30% in a single day. In addition, as a new pledged asset, sUSD's weight distribution mechanism in the verification node's collateral has not yet been made public. If it is excessively associated with SOL and sSOL, it may cause the Solana verification node's collateral concentration to exceed the standard, which will instead weaken the decentralization and security of the network. 5. Future Outlook: Exploring the Path to Scale amidst Challenges In the long term, sUSD's development potential coexists with risks, but industry trends provide it with important opportunities: the size of the re-hypothecation market is expected to exceed US$10 billion by the end of 2025, and the RWA market will continue to expand, and Solayer has included "zero-knowledge proof integration" and "cross-chain alliance expansion" in the 2025 roadmap - zero-knowledge proof can improve the privacy and audit efficiency of RWA assets, and cross-chain expansion can allow sUSD to break through Solana Single chain restriction, becoming a cross-ecological RWA stable currency. If Solayer can gradually solve core issues such as compliance qualifications, asset transparency, and liquidity reserves, sUSD is expected to occupy a unique position in the stablecoin track by virtue of its differentiated advantages of "income + pledge + ecological synergy", and even reconstruct the value anchoring system of the Web3 world - from "encrypted asset mortgage" to "real asset support", and from "single function" to "multi-scenario empowerment". However, in the short term, we need to be alert to risks such as regulatory policy changes and market liquidity shocks, and find a balance between innovation and compliance, scale and security, in order to achieve sustainable development. |

|

|

|

|

|