English

English20917

[Full text is generated by AI]

1. BTC is now in the "fluctuation period in the second half of the bull market" (it may be a period of shock and decline, which is more likely - author's note)Let’s talk about the conclusion first: The current (November 2025) BTC position is most similar to the position from the fourth quarter of 2020 to the first quarter of 2021, but the pace will be slower. (It looks like the macro environment, but market expectations have been completed) Why do you say that? 1. Macro position: from “to be loose” to “not really wide yet””

That is to say: 👉 This is not the top range, but this is the range where you need to be able to "do swings". This is no longer the stage where you can earn 10 times a year with your eyes closed.   2. Which period is most similar to history?

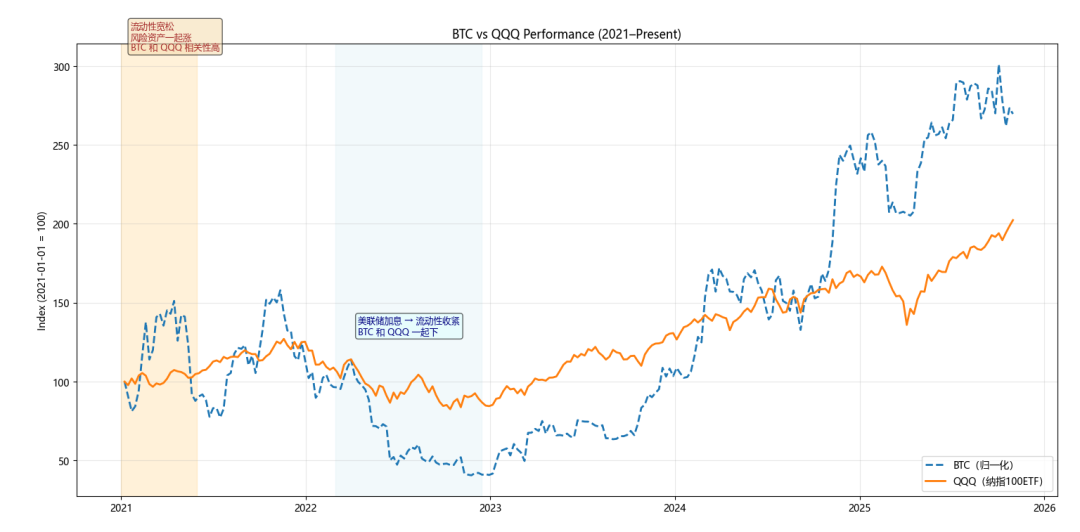

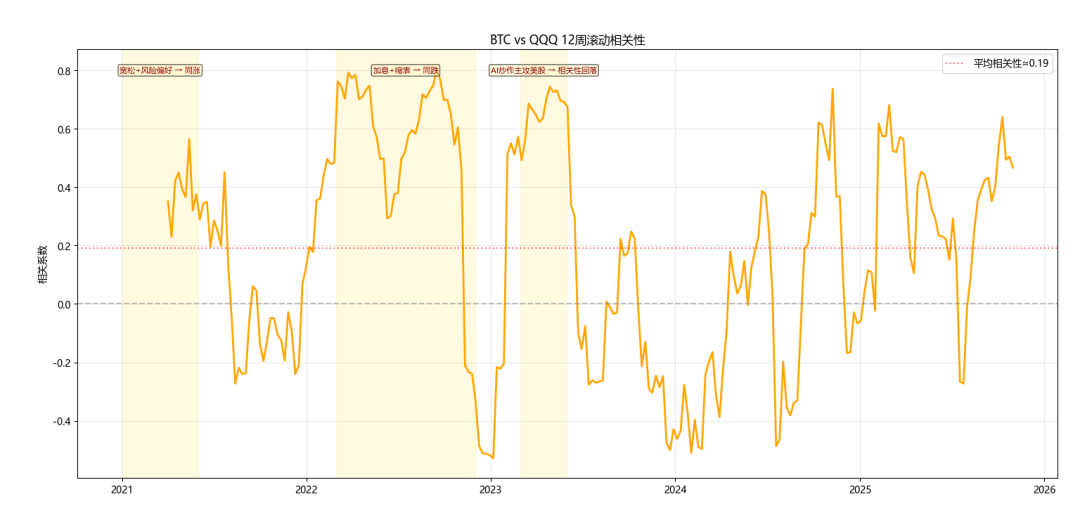

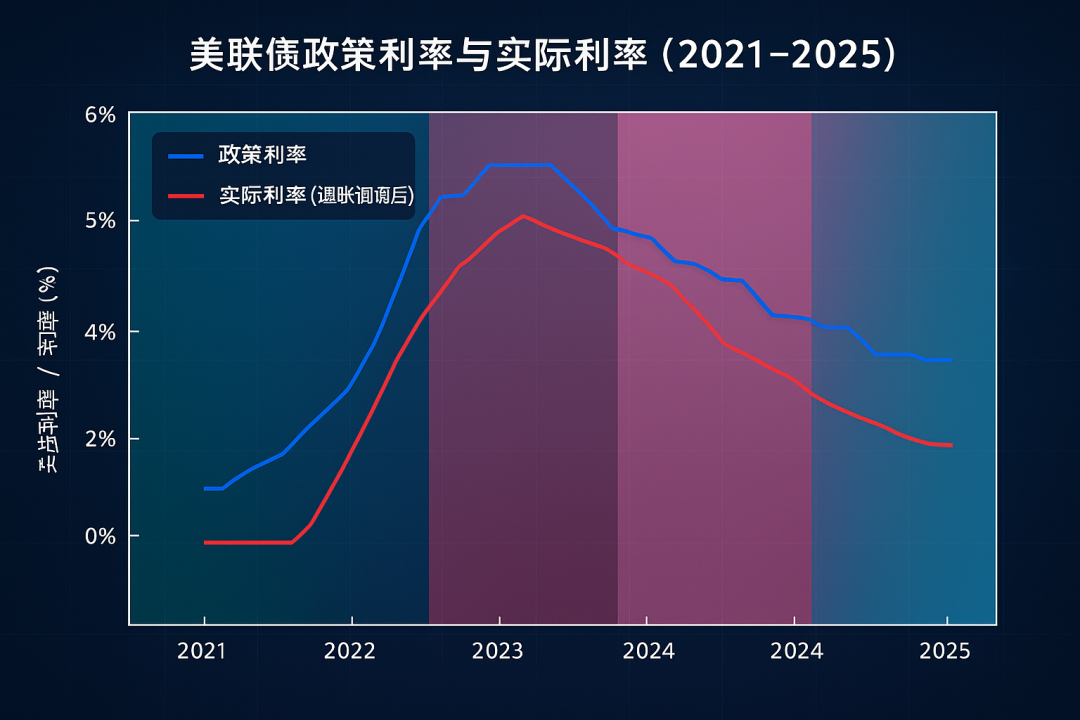

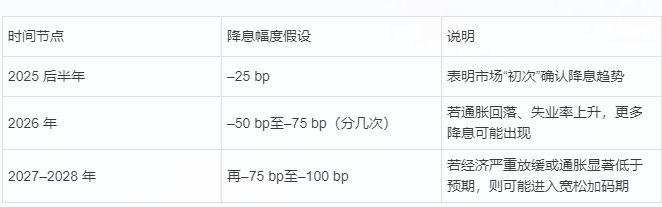

So we can give this stage a name: “The high turnover period after the bull market (pre-easing stage)” General direction: 🟢 Medium-term fluctuations, if there is no room for interest rate cuts in the future, it may be at the end of the bull market. Fluctuation: ⚠️ getting bigger Method: ❌ Not suitable for mindlessly taking full positions Suitable for: ✅ Do "sell high and buy low + keep core positions based on momentum and short cycles"” 2. Expectations of future interest rate easing in the United States Okay, let’s do a qualitative + quantitative deduction together: what is the current pace of subsequent interest rate cuts by the Federal Reserve (Federal Reserve), and what is the possible downside to the 30-year U.S. Treasury bond yield (hereinafter referred to as the “30 Y yield”) if the rate cut is really implemented gradually. ----------------------------------------------------------------------- 🔍 Overview of current situation - The current 30 Y yield is about 4.6% (recent data is 4.58%) (fred.stlouisfed.org). - The Federal Reserve's policy interest rate (federal funds rate) remains at a high level, and although inflation has eased, core inflation remains highly sticky. - At the same time, although the market expects an interest rate cut, the "real interest rate cut cycle" has not yet fully started. - Long-term bond yields are not only affected by policy interest rates, but also by "inflation expectations + real interest rates + term premium". (fredblog.stlouisfed.org) -------------------------------------------------------------------------------- 📉 Assumptions about the pace of interest rate cuts We assume that the Federal Reserve will gradually start cutting interest rates in the future, based on the following possible paths:  In other words, the policy interest rate may fall from the current assumption of ~5% (assumed value) to around ~3% or lower in the next 1-2 years. -------------------------------------------------------------------------------- 🧮 Quantitative deduction of the downside space of 30Y yield 30 Y yield ≈ expected average short-term interest rate + inflation expectation + term premium. We assume that during a rate cut cycle, all three move in a direction that favors falling yields. Hypothetical variables - Expected short-term interest rates average: currently assumed to be ~4.0%, falling to ~2.5% in the future. - Inflation expectations: currently assumed to be ~3.0%, falling to ~2.0% in the future. - Term premium: currently assumed to be ~0.5%, may fall to ~0.2% in the future. extrapolate If 30 Y yield = expected average short-term interest rate (2.5%) + inflation expectation (2.0%) + term premium (0.2%) ≈ 4.7%. It is currently ~4.6%–4.7%, which is actually close to the above-mentioned hypothetical state. But if the market further believes that inflation will fall to, say, 1.5%, real interest rates are expected to fall, and the term premium also falls further, then: - Expected average short-term interest rates: 2.0% - Inflation expectations: 1.5% - Term premium: 0.1% Total = 3.6%. Therefore, under a more optimistic scenario, the 30 Y yield could theoretically fall back to the 3.5%–4.0% range. -------------------------------------------------------------------------------- 📊 Downside summary - More conservative scenario: Yield drops from ~4.6% to ~4.0% → a decrease of approximately 60 bps. - Optimistic scenario (inflation + term premium declines rapidly): It is possible to drop to ~3.5% or even ~3.0%, but this path is more difficult because fiscal supply, inflation stickiness, and term premium are difficult to reduce quickly. - Note: If the economy performs strongly or fiscal supply becomes larger and the term premium continues to rise, yields may not go down or even rebound. The core reason why it is not the Q1 quarter of 2020-2021 is that the space for this round of interest rate cuts is restricted (completely different from the unlimited QE in 2020).3. Who is pushing and who is suppressing in the short cycle?You made a very important observation earlier: BTC has a small fluctuation cycle of about 16 days. This observation is valid. It is related to several things. Let’s take a look at them. 1. Driving force ①: “breathing” of derivatives positions”

2. Driving force ②: the rhythm of miners and long-term holders

3. Driving force ③: Macro expected eventsIn short cycles, there is another type of false breakthrough or real event:

So you have to remember one sentence: The short cycle is created by the combination of derivatives + miners + macro calendar, not by pure technology. This is why you can see the "rhythm" using ROC, but sometimes the rhythm is ahead/lags 2 to 3 days - that's because events are affecting it. 4. November → Four key points to keep an eye on before the next real interest rate cutYou asked the question correctly: This period is actually the easiest to make mistakes, because everyone knows that interest rates are going to be cut, but no one knows whether it will be this time or next time. Therefore, in this period, we need to "keep an eye on the macro trigger points + follow the technical rhythm." I’ll break it down into four points for you to focus on👇 ① Will CPI/PCE fall off a cliff?

📌 Operation suggestions: If the data in November and December are obviously leaning towards 2.x%, we will be more cautious and the top signal can be done less often. ② Dot plot / "Rhythm and tone of Fed officials' speeches"”

📌 Operation suggestions: At this time, you must resolutely follow your rule of "three days before ROC turns around" and don't be lured into long/short positions by the K-line. ③ Will long-term U.S. bond yields continue to fall?You have already asked a very professional question: "Why did the 30-year U.S. Treasury bond fall so slowly from 4.6%?" ” This is the third point to look at in this paragraph:

📌 Operation suggestions:

④ Have ETF/institutional buying orders come back?This step is actually to see whether incremental funds have really come in.

📌 One sentence version: There is an increase → you can get it; No increment → only bands. 5. What to expect? (Give a more realistic road map)Let me help you draw the most likely path (of course the one with the highest probability):

6. The last sentenceToday's BTC is not a question of whether to buy it, but a question of "can you survive in the period of high volatility and use rules?" The real flood will have to wait until the point when "continuous interest rate cuts are confirmed + long-term interest rates will also go down." Until then, just use your "top/bottom ROC model" and eat one piece at a time. This is the most reasonable way to play. |

|

|

|

|

|

【Depth】The crossroads of Ethereum (ETH): The 1-hour K-line

Ethereum’s quantum upgrade

ETH seems to be stabilizing, but it is actually a false fire

Solana Foundation Recruitment!

sol market analysis on March 24, 2026

SOL market analysis 3.23

BNB is about to make a comeback!

The most stable method of ETH is exposed tonight!

2026-03-26

2026-03-26

2026-03-26

2026-03-26

ETH

ETH