English

English66711

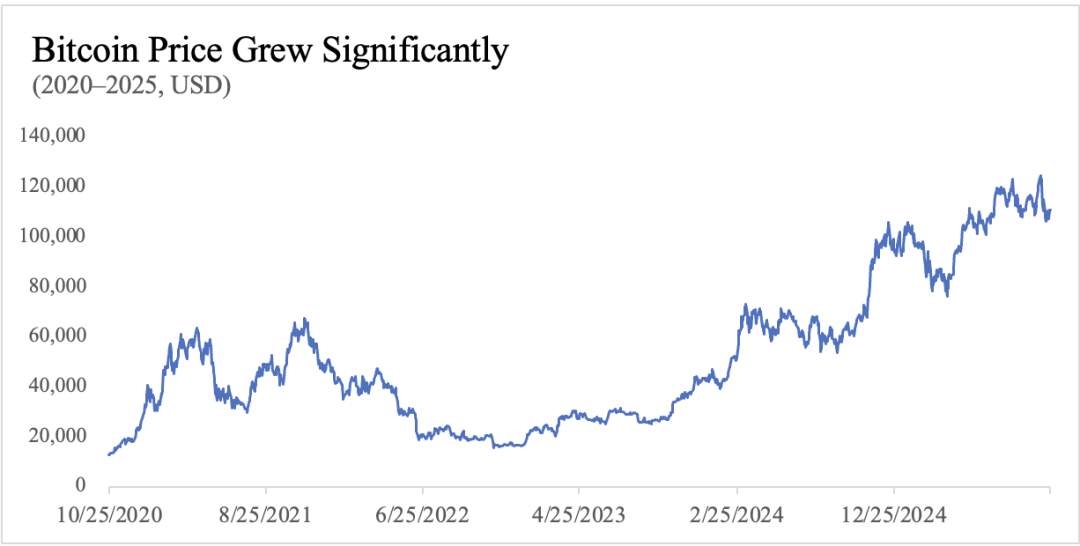

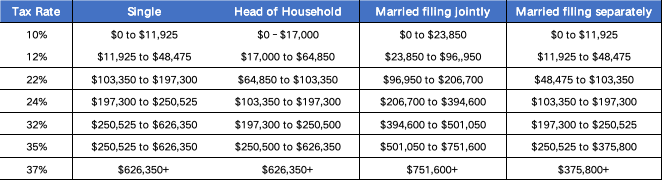

1. Bitcoin price surges In recent years, Bitcoin prices have experienced multiple rounds of strong increases. At the beginning of 2023, the price of Bitcoin was only about US$20,000. Now, the price of Bitcoin has already exceeded the US$100,000 mark and has remained high for a long time, with the price almost fivefold. Bitcoin's continued rise over more than two years reflects the global liquidity environment, institutional allocation needs, and the trend of digital assets entering the mainstream financial system.  Data source: yahoo finance, chart FinTax homemade  Add FinTax CEO Assistant immediately to experience the enterprise-level cryptocurrency financial suite FinTax Suite, which realizes real-time encryption asset integration and tracking, easily copes with high-frequency transactions and market fluctuations, and generates various financial statements to meet the daily management and auditing needs of institutions!  2. High income comes with high tax burden However, the other side of the price surge is the real problem faced by Bitcoin investors when they liquidate - with the tightening of tax regulations in various countries, the income tax on BTC liquidation is under great pressure. Taking the United States as an example, the IRS treats cryptocurrencies as assets. Therefore, when cryptoassets are sold, traded, or disposed of, their income will be treated as capital gains or ordinary income and taxed at the relevant tax rates. Specifically: If a cryptocurrency is held for less than a year, short-term capital gains tax is payable at ordinary income tax rates, which vary based on an individual's annual income and range from 10% to 37%. The federal income tax rates for tax year 2025 are:  Long-term capital gains tax is payable if you hold cryptocurrencies for more than a year, and long-term capital gains are subject to reduced rates. Most taxpayers will pay a tax rate of 0%, 15% or 20%. The long-term cryptocurrency income tax rate in 2025 is:  3. New tax planning ideas based on accelerated depreciation policy However, greater tax pressure does not mean that taxpayers completely lose planning space. If you make reasonable use of the provisions of the U.S. tax law system, you can still reduce the effective tax burden under the premise of compliance. For example, the “accelerated depreciation” policy stipulated in Section 168(k) of the U.S. Tax Code allows taxpayers to deduct the entire cost of fixed assets such as mining machines or servers at once in the year they purchase them, thereby significantly reducing the amount of income payable. Its specific provisions are as follows (k)Special allowance for certain property (1)Additional allowance In the case of any qualified property— (A) the depreciation deduction provided by section 167(a) for the taxable year in which such property is placed in service shall include an allowance equal to 100 percent of the adjusted basis of the qualified property, and (B) the adjusted basis of the qualified property shall be reduced by the amount of such deduction before computing the amount otherwise allowable as a depreciation deduction under this chapter for such taxable year and any subsequent taxable year. Let’s take a simple example to describe the effect of this tax financing method: an American mining company will receive an income of US$1 million in 2024 and invest US$500,000 in purchasing mining machines that year. Assume the corporate income tax rate is 21%. If the §168(k) accelerated depreciation policy applies: the company can deduct the entire cost of $500,000 in one lump sum in the current year, and the income tax is approximately: (100−50)×21%=$10.5 million If normal depreciation is used, such as five-year straight-line depreciation: only US$100,000 can be deducted each year, and the income tax is approximately: (100−10)×21%=$18.9 million It should be noted that when using the accelerated depreciation method, you need to consider the cost situation of the year to avoid loss of profits and subsequent carryover losses. Here is another simple example: an American mining company still invested US$500,000 in purchasing mining machines in 2024, but received US$400,000 in revenue that year. If the §168(k) accelerated depreciation policy is still adopted: The company can deduct all US$500,000 of costs in one lump sum that year, but due to low revenue, it will form a book loss of US$100,000 (NOL, Net Operating Loss) after deduction. Although profits for the current period are negative and no income tax is payable, this also means that the company cannot withdraw or distribute profits, even if there is still cash flow on the books. At the same time, in terms of tax treatment, according to current regulations, NOL carried forward to the next year can only be deducted from 80% of the taxable income of that year, so it is not wise to blindly use accelerated depreciation in low-profit years. 4. Summary Overall, although the continued rise in Bitcoin prices has brought considerable investment returns, it has also made tax issues more prominent. Faced with the dual pressures of tighter supervision and rising tax burdens, it is not advisable to blindly avoid risks. It is a more rational choice to understand and make good use of the compliance policy provisions in the current tax law for tax planning. Take the "accelerated depreciation" policy of §168(k) as an example. It provides the capital-intensive crypto industry with a realistic path to legally reduce taxes and optimize cash flow. This case also shows once again that systematic planning within a compliance framework and using the space of institutional design to resolve tax burden dilemmas are the key ideas for cryptocurrency investors to achieve sustainable development.   The information or articles published on this official account are only for communication and discussion or general reference purposes. Any content on this official account should not be regarded as regulatory, tax, accounting, investment or other professional consulting advice, nor does it represent a recommendation or offer for any services or products. This official account does not make any express or implied representation or warranty as to the accuracy, completeness or reliability of the information. This official account will not notify any changes to any published content, and this official account has no obligation to update any published content. FinTax does not assume any responsibility for any judgment or decision (regardless of actions or inactions) made based on all or part of the content of this official account and the resulting legal consequences. No content in this official account may be used for any other purpose without the prior written consent of FinTax. Please obtain authorization for reprinting and indicate the author and source "FinTax". |

|

|

|

|

|

【Depth】The crossroads of Ethereum (ETH): The 1-hour K-line

Ethereum’s quantum upgrade

ETH seems to be stabilizing, but it is actually a false fire

Solana Foundation Recruitment!

sol market analysis on March 24, 2026

SOL market analysis 3.23

BNB is about to make a comeback!

The most stable method of ETH is exposed tonight!

2026-03-26

2026-03-26

2026-03-26

2026-03-26

ETH

ETH