English

English23586

Markets price down December rate cut; Bitcoin could be more stable than altcoins by 2026.  The Federal Reserve just cut its policy rate by 25 basis points, moving the target range to 3.75% to 4.00%. However, futures markets have now eliminated the prospect of further rate cuts in December. Ahead of yesterday's FOMC meeting, many traders expected a third rate cut as inflation has gradually eased, the labor market has shown signs of weakness and the Fed has begun to ease. While the Fed did cut interest rates this time, Powell stressed that another rate cut in December is "not a done deal, far from it." Powell said.

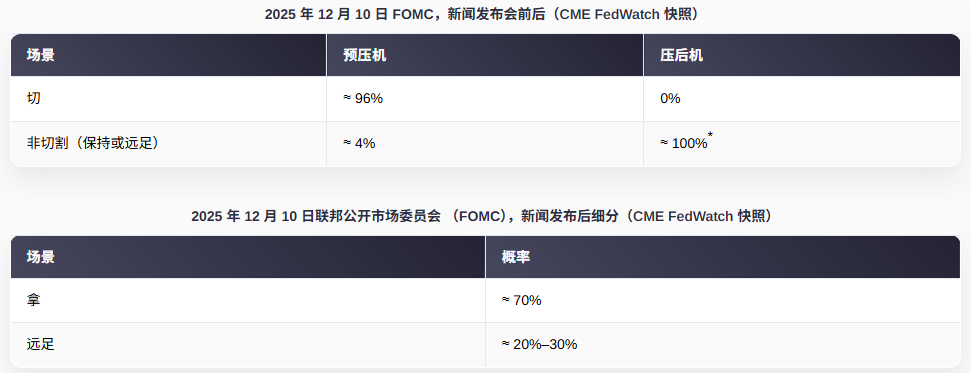

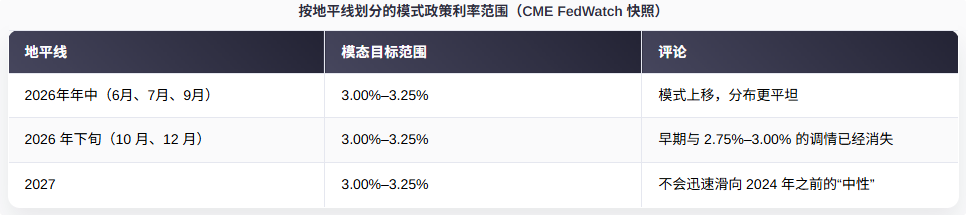

After the press conference, as the base case with a real-time rate hike tail, the odds shifted from an all-but-locked additional rate cut to on hold, with the interest rate path distribution rising and flattening in 2026, according to CME FedWatch data. This adjustment leaves cryptocurrencies facing a stickier liquidity backdrop, tighter sensitivity to incoming macro data, and wider dispersion among coins.  January 2026 remains on the tail end of a rate hike near 18.5%, according to FedWatch data, reflecting lingering concerns that sticky inflation could pull the committee toward a reversal if data does not cool.  The long-term path reprices higher. By 2026, the FedWatch distribution shifted a total of about 25 basis points upward and leveled off, with model results clustered around 3.00% to 3.25% by mid-to-late 2026 and continuing into 2027. Previous snapshots suggested a tilt toward 2.75% to 3.00% by the end of 2026. The profile implies fewer rate cuts, with markets pricing in a higher neutral real rate than earlier estimates.  Direct market interpretation of cryptocurrencies relates to liquidity and interest rates.A longer-term higher stance supports the dollar and keeps real yields firm, which tends to weigh on high-beta risk and longer-term narratives related to long-term cash flows. Bitcoin tends to absorb this impulse with less retracement than smaller market cap coins and alt-L1s. However, broad cryptocurrency liquidity, including stablecoin floating and perpetual leverage, still reflects the same macro environment. As balance sheet drains continue and policy rates rise, the cost of capital within the crypto ecosystem remains constrained, with Treasury alternatives pulling some marginal demand out of basis and spread structures. Streaming becomes more data dependent. Spot ETF and fund allocations are sensitive to rate hike tail swings around major data. Upside inflation or red-hot labor data tend to increase the likelihood of near-term rate hikes and stress risks, while overt deflation could reopen demand for duration and growth proxies. As probabilities move, this environment favors faster rotations between BTC and altcoins, with allocators favoring higher quality balance sheet and liquidity pairs when uncertainty increases. Policy uncertainty also reshapes volatility regimes. A thicker rate hike tail widens the spread of crypto return outcomes, with correlations to real yields and the USD Index typically rising into key macro releases. This model can increase decentralization within cryptocurrencies, with projects based on more precise cash flow or fee capture better able to maintain than tokens with long-term token economics and large emissions. As the risk-free anchor rises, funding markets are likely to depreciate, with miners facing higher capital expenditures and future cash flow discount rates, raising concerns about power costs, leverage and funding mixes. Scenario mapping for the next one to three months centers on three paths. The base case is that the odds are close to 70% in December in the latest snapshot, with growth cooling and inflation not yet weak enough to warrant another rapid rate cut. In this setup, real yields remain firm, stocks and cryptocurrencies trade range-bound, and BTC's performance favors resilience with high-beta alt exposure. A hawkish surprise, defined as a 25 basis point upward move from the 20% to 30% tail in December or January, would amplify risk-off pressures, boost the USD, and compress long-term cryptocurrency valuations, increasing drawdown risk in leverage-intensive segments while driving flows to cash flow infrastructure and quality L2. The dovish surprise and core indicators fading convincingly will put rate cuts back to pricing in mid-2026. The liquidity impulse will first lift BTC as the cleanest macro proxy and then expand if the soft landing narrative strengthens. Portfolio construction in this tape typically prioritizes liquidity management, basis calibration, and convexity. Given its depth and cleaner macro beta, BTC remains the most direct tool for expressing changes in policy odds around CPI, PCE and labor report tactics. In alternative investments, dispersion screening, emissions, and fee capture around the runway are more important when the risk-free anchor is higher. For miners, sensitivity to power pricing and balance sheet leverage becomes a bigger driver of equity-linked tokens and revenue sharing, with forward hedging costs needing to be weighed against spot upside options.

Repricing is visible across the entire meeting outcome curve, with the December 10 meeting now taking no action as the base case and proposing a non-trivial rate hike tail, according to CME FedWatch data. According to the Fed, benchmark actions delivered rate cuts, while communications kept the easing path slow and conditional. The December meeting is now in focus, with the odds on hold being the centerpiece and a real-time rate hike tail emerging. Thank you for your attention and learn more about encryption! ! ! Recommended reading: Ethereum LTH hits 3-month high amid October sell-off WLFI’s token will be listed on Binance US, will the price surge? US Secretary of State hints at positive trends in Sino-US trade, BTC price breaks through $113,000 Bitcoin accumulation pattern shows late-cycle maturation, not clear end ETH Sharks and Whales Are Back: What Does This Mean for ETH Price? SOL price expected to make a comeback as pledged Solana ETF funds surge |

|

|

|

|

|

【Depth】The crossroads of Ethereum (ETH): The 1-hour K-line

Ethereum’s quantum upgrade

ETH seems to be stabilizing, but it is actually a false fire

Solana Foundation Recruitment!

sol market analysis on March 24, 2026

SOL market analysis 3.23

BNB is about to make a comeback!

The most stable method of ETH is exposed tonight!

2026-03-26

2026-03-26

2026-03-26

2026-03-26

ETH

ETH